A newsletter on mental models to help marketers do better and be better. If you like it, you can subscribe. You can also read newsletter archives and long form essays on marketing here.

As someone whose default thought process is to challenge status quo, my antenna are sensitized to disruptive ideas. I am also a huuuge fan of behavioral economics.

So when I learnt how Lemonade are using behavioral economics to challenge 125yr old insurance behemoths, I had to write about it.

At a high level, this is how the business model works. We pay monthly premium in return for a promise by the insurance company, that we can claim losses we may incur from adversity. All premiums are pooled to pay future claims. Since the insurance company does not want this money to stay idle, it invests it.

But we know that only a small percentage of us end up raising a claim. This gives huge financial leverage to insurance companies and they continue to grow wealthy as their investments compound.

In fact Warren Buffet started building his wealth via insurance. He believes this asset class is bullet proof and prefers it over other asset classes. Here is a newspaper article he wrote 20 years ago.

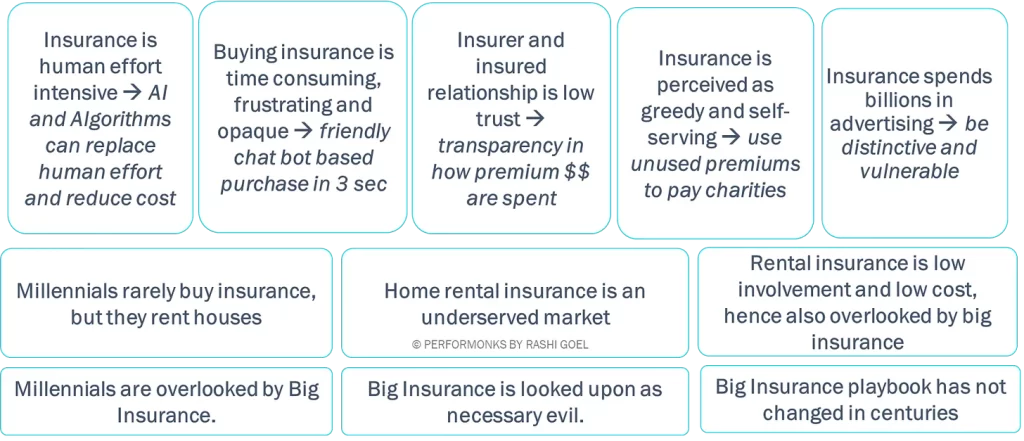

So the business model incentivizes Insurance giants to deny claims on one hand and reduce operating costs by favoring high value items like houses, cars etc. over low value items like pets and bikes. This has created a combative and mistrustful relationship between big insurance and consumers.

Lemonade does the opposite. They do not earn from investing unpaid premiums. Instead, they keep costs low and earn a flat fee on each insurance policy. This keeps their business model clean. So they insure even low value items and pay out claims within minutes. They have been successful with this new model, and have served 1mio customers in 5 years, with ~$1bio revenue.

To do this, they broke every rule in the centuries old playbook.

- Target audience: Serving future consumers, alienating everyone else

- Experience: Tech enabled service replacing insurance agents

- Social Good: Converting necessary evil to social good

- Low cost marketing: Marketing that makes insurance ‘cool’

Serving future consumers, alienating everyone else

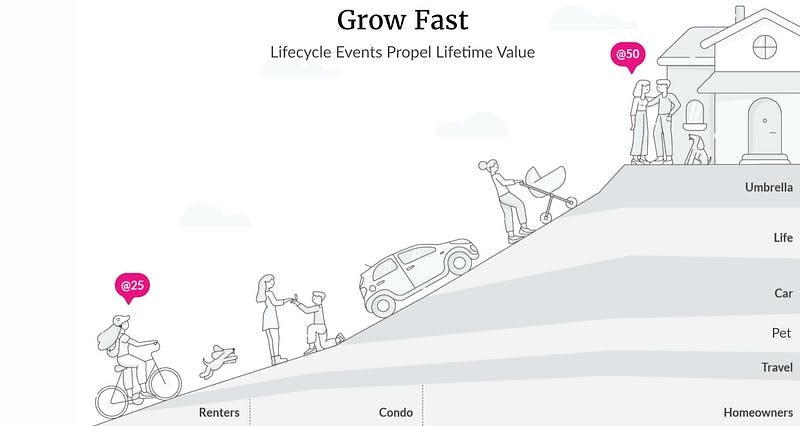

Big insurance doesn’t talk to Millennials, therefore it does not insure low value products. But most of Lemonade’s consumers are under 35 and first time insurance buyers of home rentals and pets, with premiums as low as $60.

For Lemonade, millennial is less of a demographic, but more of an attitude – people who embrace the transformative power of technology. Lemonade is so sharp focused on this audience, that it purposely alienates the traditional insurance buyer.

This also a future ready business, because today’s millennials are tomorrow’s high net worth insurance buyers.

Tech enabled service replacing insurance agents

Big insurance is an analog world. The user experience involves agents, reams of complex paperwork and hassle. Lemonade is an InsureTech company, therefore it is Direct to Consumer. It uses bots and tech algorithms to process policies within just 3 seconds to 24 hours!

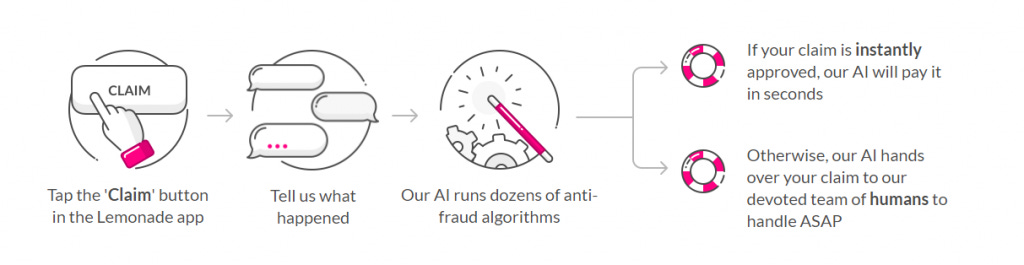

Quick Claim settlement

Unlike big insurance, claims are processed hassle free. Pictures and videos of damages can be uploaded directly on the app. And claims are sent directly to debit cards within seconds.

No complex legalese

They have also crowd sourced (!) the policy document, and made it simple, free of opaque legalese and more human.

Here is a longer video that explains the end-to-end process.

Converting necessary evil to social good

Social good is important to millennials. While big insurance is seen as a necessary evil, Lemonade, bakes social good right into its business model.

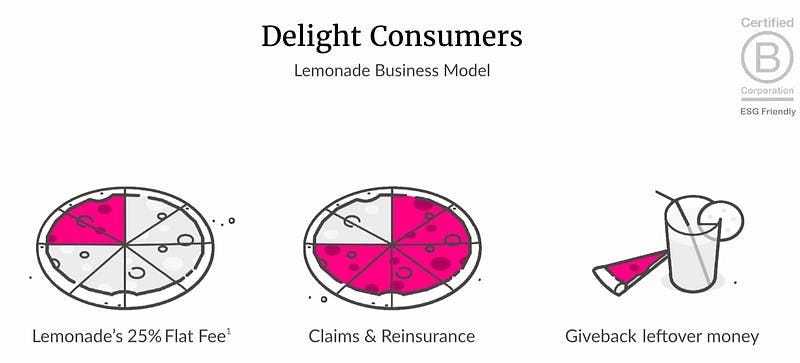

Lemonade earns a flat fee of 25% per cover, so it has no incentive to deny claims. Any unclaimed premium is donated to charities picked by consumers. Lemonade’s consumers know that if they make fraudulent claims, the money is taken from their chosen charity, not from Lemonade.

This visual shows the Lemonade business model.

This virtuous circle fosters trustful relationships between insured and insurer.

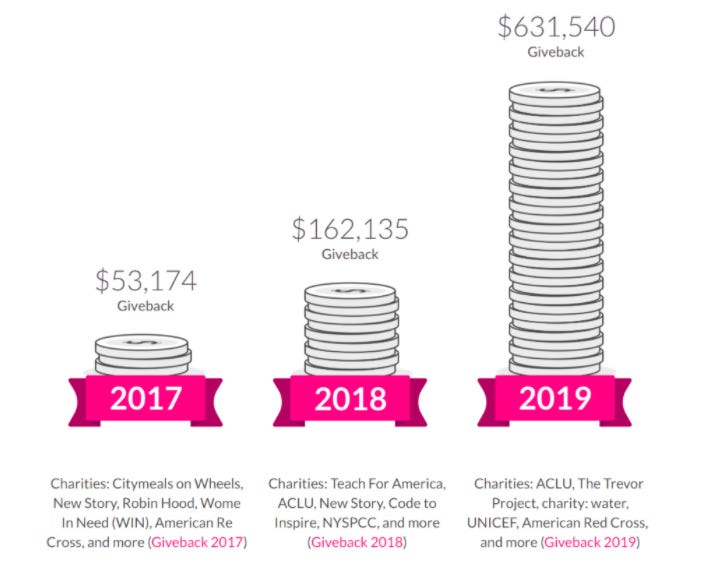

Lemonade Givebacks have only grown in the last few years.

Insurance industry is built on a foundation of mistrust. The highest NPS score any big insurer gets is ~20. Lemonade has an NPS rating of 70.

Marketing that makes insurance ‘cool’

The industry invests a lot of money in human interaction, to make the sale. The challenge for Lemonade was to win trust as a face-less App. But they ended up doing more than that.

They made insurance cool.

The Name

Who in their right minds names an insurance company “Lemonade”? Doesn’t it sound juvenile? Incompetent? They took the risk. And it worked. For one, it signaled the difference between them and big insurers. It appealed to millennials who shy away from self important behemoths.

But the name by itself would not have worked, were it not for the simple, transparent and even vulnerable marketing tone and manner.

Vulnerability

To be vulnerable is to be human. Lemonade was transparent from day one. They publish performance numbers freely, share multiple examples of negative feedback, publish a blogpost saying, We suck, sometimes. What insurance brand would admit that “our underwriting was pretty shoddy in our early days”?

Lemonade’s communication style mirrors the easy breezy product experience and supports the picture of a trustworthy, transparent, humane brand. They even discuss internal restructuring and KPIs openly on their blog. As a customer, it’s easy to feel like a part of the Lemonade community.

Visually stunning social media

This Instagram feed does not look like it belongs to an insurance player. Their signature magenta color scheme adds color to a drab industry and their content adds quirk that appeals to millennials.

I have covered how Lemonade went about their social media strategy here.

Cheaper Marketing

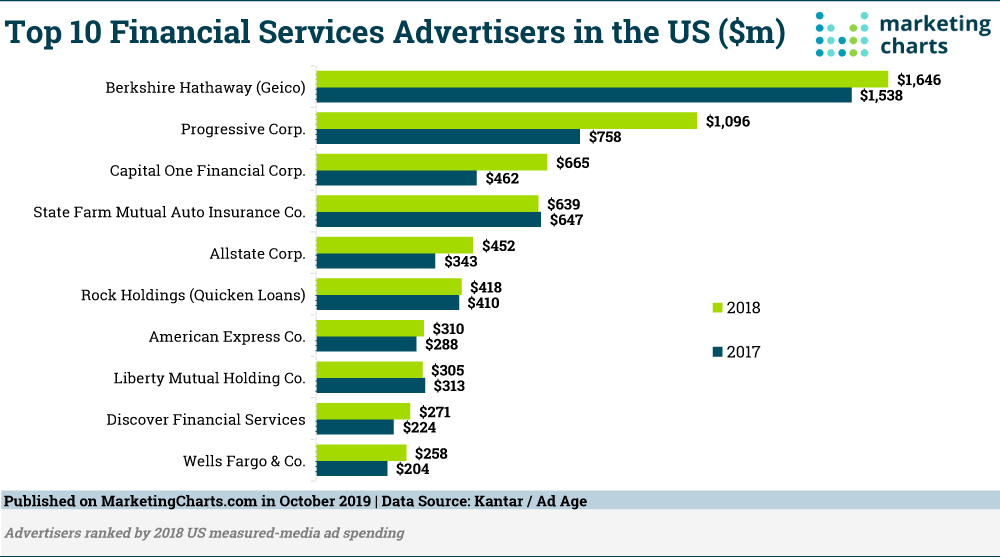

Extravagant marketing in a low trust industry sends the wrong signal – of pockets lined with consumer dollars. Big insurers spend billions of dollars in marketing. Lemonade spends billions less. They spent only $57.9 million in 2020.

What I learnt

This is the Lemonade playbook summarized, read bottom up to see the industry fundamentals that were overturned by Lemonade:

- There are no holy cows. Insurance has been successful for centuries. Longevity does not guarantee future success.

- Don’t disrupt for the sake of disruption. Lemonade did not wake up one day and decide to be a bull in a china shop. Each element of disruption emanated from deep consumer knowledge of tech savvy millennials and complete conviction that old insurance is broken and needs to be fixed.

- Disrupt completely. Once the logic to disrupt is in place, don’t be half-hearted about it. Go all the way. I have written about the ‘systems view of marketing’ here, here and here. It means every part of a company is interrelated, and a change in one function has a knockdown effect across the entire organization. Lemonade stayed true to the disruption gene across all functions.

- Deep homework makes it look easy. Lemonade has worked so hard to perfect the consumer experience, that they make it look effortless. For instance, they have data heavy algorithms [rental rates, safe neighborhoods, market movements etc.] in the background so they can generate a premium calculation within seconds.

- Secret Sauce. Behavioral economics is the new consumer insights function. Renowned behavioral economist Dan Ariely advises Lemonade. Every element is designed to win trust and be humane.

That’s all for today…

Stay inspired!