In the early days of FMCG, before trains were air-conditioned and before anyone in India had heard the word bank account, a sales officer would have a *Permanent Journey Plan (*PJP), of 25 towns each month.

He would send a postcard to distributors across these 25 towns, alerting them to his train arrival time.

At each station, the local distributor would receive him – tea, samosa, and an order sheet in hand.

The distributor took extra care of the sales officer, to make sure that his order was supplied on time.

Every few months (or six), depending on the size of the town and the company’s sales force budget, the cycle would repeat1.

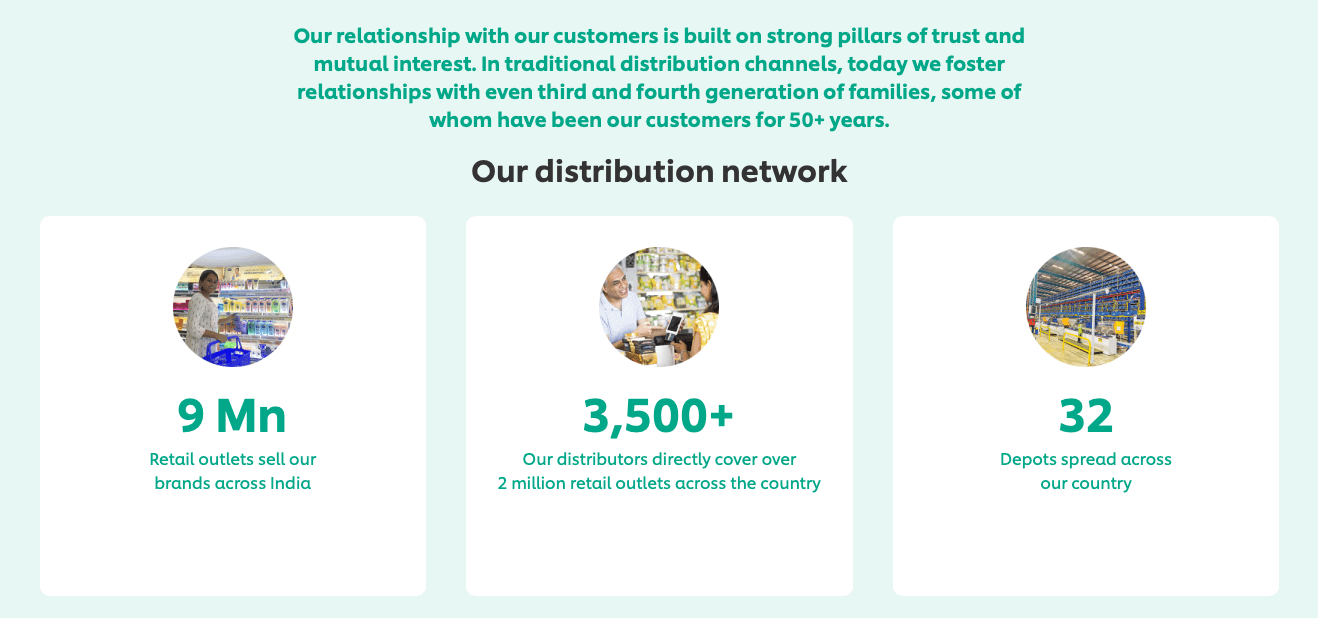

These were the earliest days of distribution in India and today, HUL has a 75 year head start.

So much so that distribution is it’s strongest moat – if HUL’s distribution spine were a river, it would be India’s Amazon.

(The river not the company).

Cut to 2026

Even the Amazon changes course.

In February, at CAGNY, Fernando Fernandez, Unilever’s CEO said 3 things about HUL.

- India is one of two “anchor” markets (alongside the US), and it should grow from 33% to 45% of global revenue.

- Quick commerce will grow from 3% to 10-15% of HUL’s revenue.

- HUL is rolling out a programme called Samadhan, which would bypass its own distributors and deliver directly to kirana stores in under 24 hours. It’s very own Amazon Prime equivalent, but for trade.

A non-strategic summary of his statement would be, “D2C gets more than 50% of their turnover on E Commerce, HUL gets only 3%, so HUL is reengineering logistics for Q Com”

The strategic reading is, “This is financial reengineering to grow HUL to 45% of Unilever’s turnover while generating cash to fund q-commerce“

The thesis: digital commerce has fragmented distribution ecosystems

This is how it plays out.

1. Distribution is not just a physical availability moat.

It also generates demand, builds brand trust, and allows consumers to discover new brands.

All through repetition.

- Availability: Simply being present in a shop is a mark of trust, because the consumer knows her kirana waala (retailer) will not stock ‘bad’ products.

- Visibility : When she sees products displayed neatly on the shelf, her trust in the product grows even more.

- Repetition: Repeated exposures like this continue to grow trust and awareness until the ‘product’ becomes a ‘brand’.

Discovery: This continues until one day she discovers a new brand on the shelf. And if the retailer recommends it, she might even buy it.

The thing is that HUL compounded this cycle for 75 years, because 8 out of 10 new brands she discovered were HUL’s!

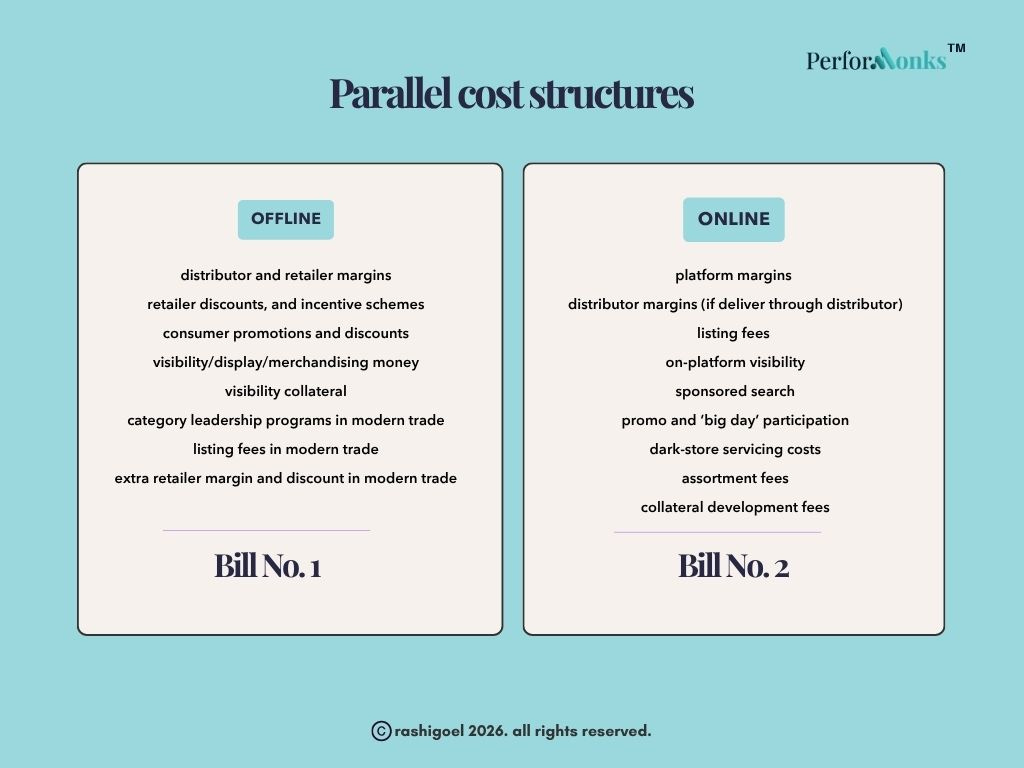

2. Digital commerce has disrupted this age-old moat.

Offline distribution is a smooth relay race, in which an army of sales leaders and merchandisers exchange margins as they pass the baton along the availability-visibility-discovery flywheel.

But digital commerce has unbundled all three, and sent over a bill for a parallel set of expenses!

3. Digital commerce not only impacts the cost.

- Fragmented spends: Anyone who has bought stuff in bulk knows that the biggest buyers get the biggest discounts and priority care. But if HUL’s wallet gets fragmented across kirana stores, modern trade, and different categories in digital-commerce, even though it still has the most funds in FMCG, its relative buying clout decreases.

- Consumer have become addicted to discount: digital commerce has trained consumers to only buy on discount, which slices margins off even more.

4. It also changes how shoppers discover and buy brands.

- Digital commerce expands brand width, which removes HUL’s monopoly: The digital commerce flywheel promises a wide range of brands. So despite HUL’s still powerful clout, they will continue to promote smaller, newer brands. To offset this, even HUL will need to spend more on visibility and search.

- Consumers shop across different channels, which means HUL must keep investing in all channels: the same consumer may buy their regular shampoo on Amazon, a conditioner they ran out of on Blinkit, but prefer to pick up a new dandruff care shampoo at their chemist store. So, HUL cannot exit any channel yet. They must continue to feed all channels until a vast proportion of the population shifts to modern trade and online. Which will take a long time in India.

- Shopping has become a game of discovery and discount, which means preference alone is not enough: If the consumer types your brand name in the search bar, there is a high likelihood that they will buy you. But if your discount is lower than the category, they may not. That means even HUL brands that enjoy preference have to shell out discounts. On the other hand, if your brand does not enjoy preference to begin with, then you have to spend for more discoverability on top of more discounts.

Net-net→With distribution fragmentation, selling online costs more. Even when you are HUL. Even when the brand is older than the customer’s grandmother.

Read in this light, Samadhan makes sense. It is not just logistics, but financial engineering.

By going direct to the kirana, HUL saves the distributor margin.

The fragmentation tax

Modern trade was supposed to kill HUL. It didn’t.

E-commerce was supposed to kill HUL. It didn’t.

Linkedin Gurus says quick commerce is the final nail in HUL’s coffin.

In response, HUL is making some big adjustments.

It is cutting out distributors from big cities where distribution has become commoditised and requires speed to move products from warehouses to dark stores+kiranas in less than 24 hours. Here, distributors who have spent careers, and sometimes generations, betting on HUL, are paying the fragmentation tax.

The expensive layer that builds relationships – where the kirana owner influences shoppers, or where distributors hold local clout, remains untouched.

This is the tightrope HUL must walk. How to keep 3,500 distributors who supply 70% of HUL’s turnover2 happy and engaged, while also winning the digital marketplace race.

Two ways to stay connected

- Strategy Activator Workshops — done with you.

We have a proven approach that we tailor to your context.

At the end of the process, you will have a strategy blueprint for growth. The approach has received great feedback from Harpic, Tata Salt and Tata Sampann. Click here to share your interest and I will get back to you.

- DIY Strategy Products

I am building self-serve products you can use to develop your growth strategy. Join the early list for first access.