Calcutta, 19th century

The hundi1 system lubricated the financial plumbing of Indian commerce end to end. Karachi to Rangoon, Kabul to Madras, every town that mattered had a Marwari2gaddi3, and every Marwari gaddi honoured every other Marwari gaddi’s paper.

This is how it worked.

When a jute trader in Rangoon needed to pay a supplier in Bombay, he did not lug bagfuls of coins across the Bay of Bengal. He just walked into a kuthi4 of Sevaram Ramrikhdas, handed over the cash and got a hundi in return. A few weeks later, his supplier in Bombay exchanged that hundi for cash at the gaddi in Mulji Jetha5 cloth market.

When the British started opening formal banks and introduced technologies like the money order and the telegraph which cut trade and payment time from weeks to a few hours, any outsider would have wagered that the hundi system was finished.

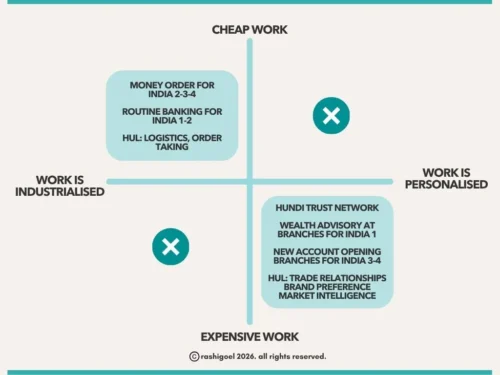

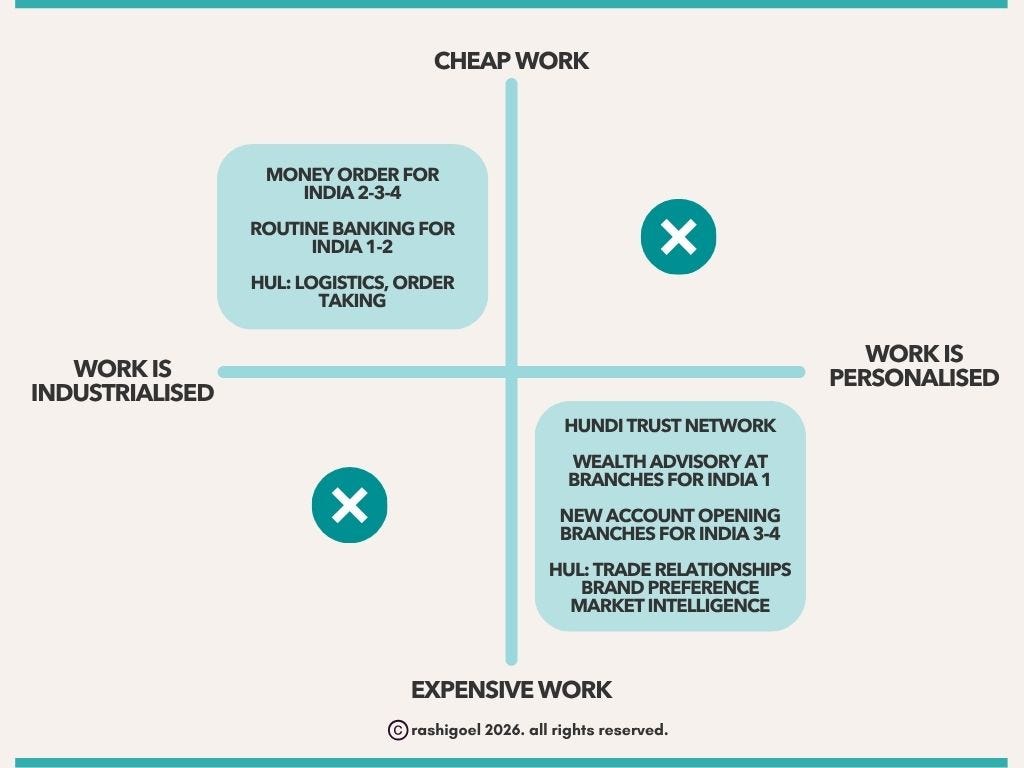

Yet, the hundi network continued to thrive because the trader community chose hard-earned trust over speed → The expensive layer remained.

On the other hand, the money order technology industrialised the cheap layer → the common man could now send small amounts of money to relatives across the country.

Modern banks, 21st century

In the 2000s, every analyst predicted that internet banking would kill bank branches.

History rhymed yet again.

The cheap layer of transactions was digitised, but branches pivoted to become strategic units that provided the expensive, trust based layer of value → wealth advisory, and relationship management to the more seasoned India 1-2.

Since India contains multitudes, the cheap layer of India 1-2 (physical branches) became the expensive value- added layer for India 3-4!

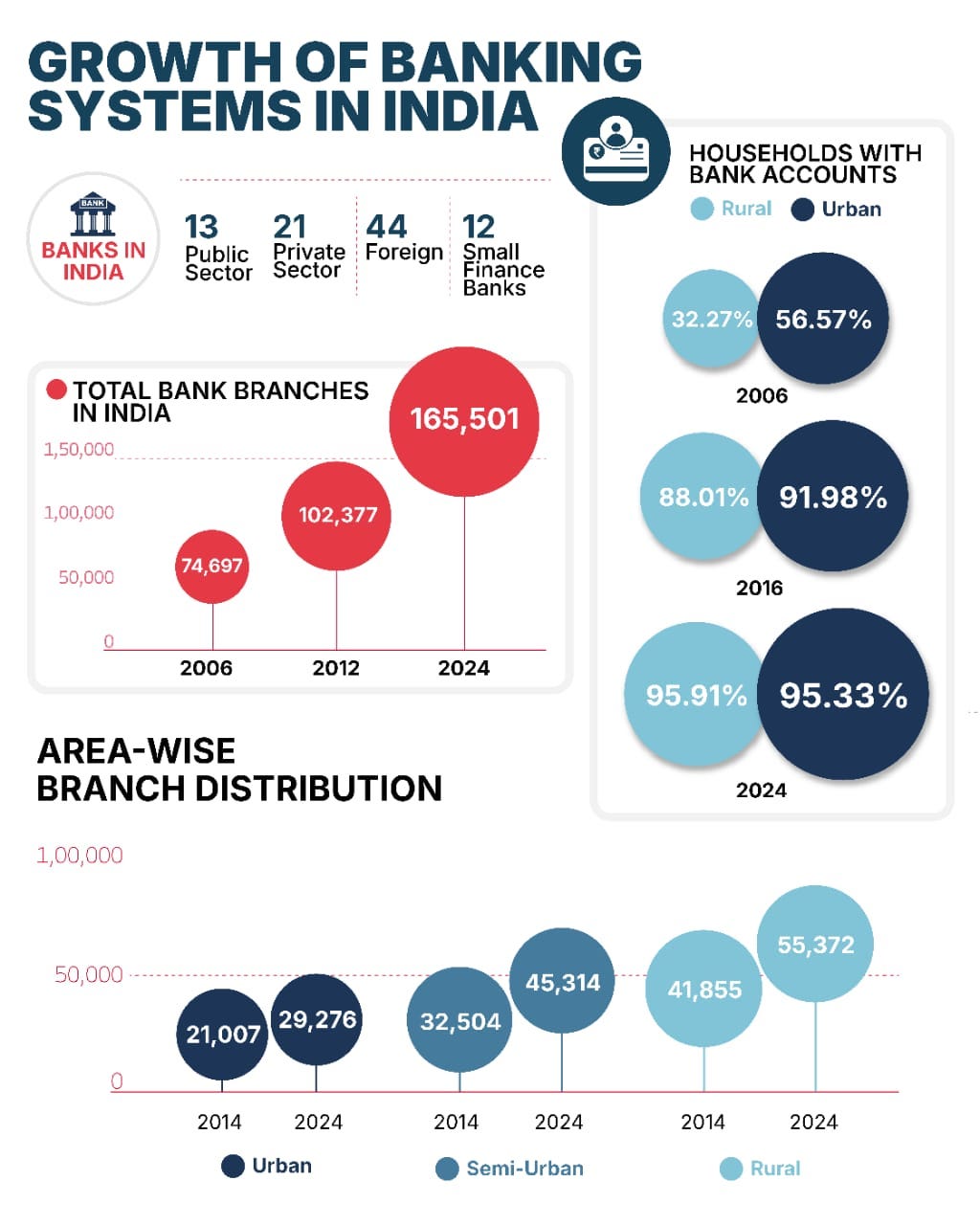

As a result, total bank branches increased to cater to the unbanked rural Indians who wanted the reassurance of a human face, as they leaped from money orders to shiny new bank accounts.

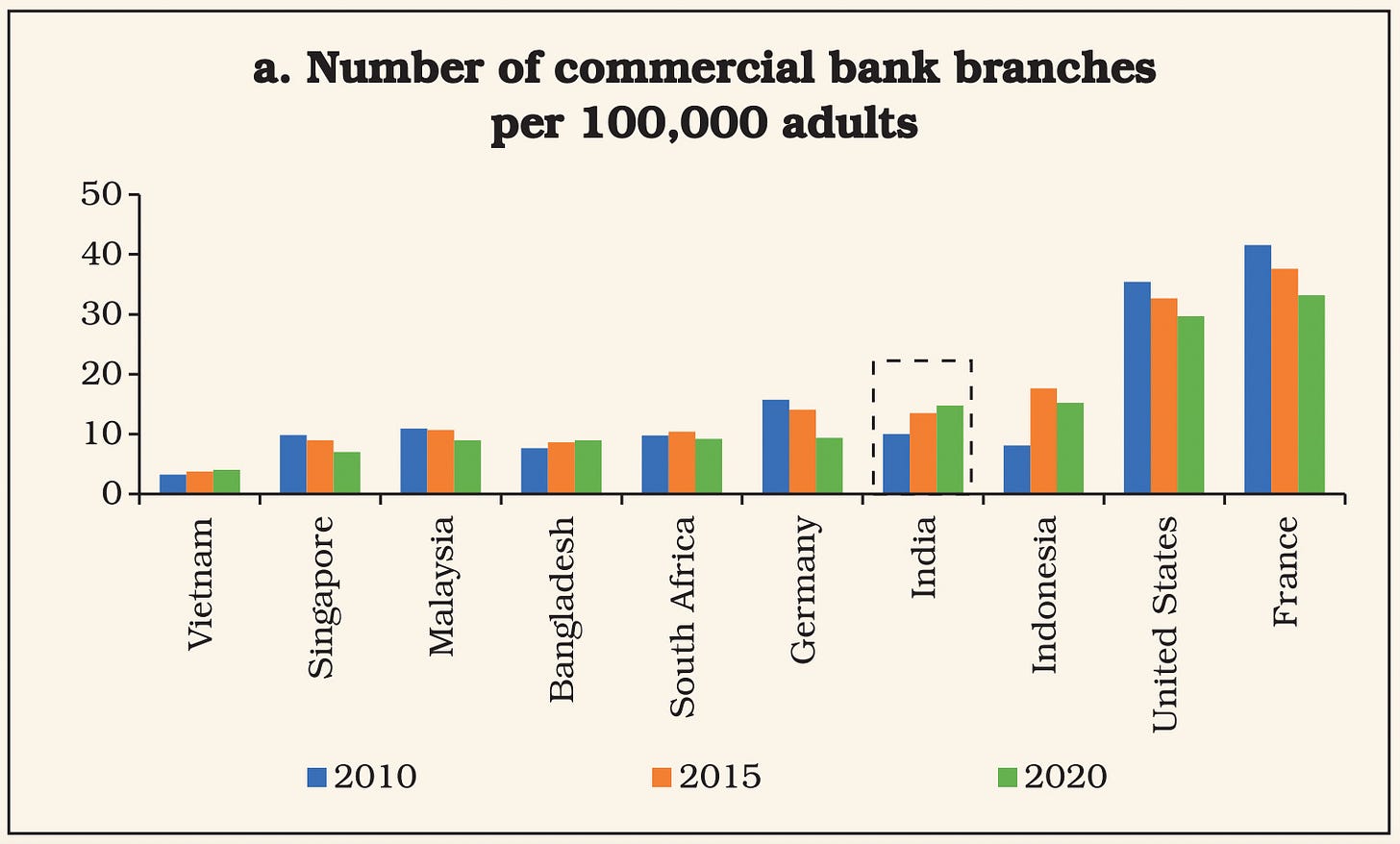

If India were a developed economy, we would have thought that’s it, post 2024, banks will start consolidating branches. But there is still more headroom to grow, because of a large underserved population.

Given the exact same context of technology, country, culture and underserved population, five different banks made five completely different strategic bets, as per Anirudha Basak’s excellent 2022 article – To Branch or Not to Branch.

Now that’s why I love strategy.

Each strategic bet came from the decision on where value lay

Each bank decided which is the cheap layer they will industrialise and which is the expensive value layer they will invest behind.

HDFC thought long-term and wanted to earn loyal customers. So they invested in an expensive grassroots distribution strategy by planning to add 1,500 to 2,000 branches per year till 2025. Their logic was that branches helped bring in more deposits, and needed to be within 6-7 km for potential customers, since no one would travel beyond that to get to a bank branch. (Reminds me of the hard work that legacy FMCG companies have put in already)

Federal Bank made the opposite bet. They outsourced distribution to fintech partnerships that brought in deposits that 2,000 new branches would have, without signing a single new lease. This smaller, scrappier bet led to discount rate-led deposits over loyalty-led. (Reminds me of D2C ‘buying’ discounted sales via digital distribution platforms)

ICICI decentralised, allowing each business head to decide branch expansion based on their local market footprint.

Kotak niched their branches to high value business customers and launched 811 – their digital product which at that time (2022), was still small, only 6% to the total deposit book.

Central Bank of India was losing money and was shutting six hundred branches.

Cut to 2026. The Great Indian FMCG Industry

FMCG today is in the same place that the Marwaris and banks were in.

Here also, we cannot mistake supply-side unbundling as the death of an institution.

Here also, value is getting reassigned.

The cheap layer of distribution, physical logistics, replenishment, order-booking, warehousing, and stock keeping will be commoditised to extract maximum value. That’s what Project Samadhan6 and Prohect Shikhar7 are doing.

These moves will improve HUL’s P&L, but when the cheap value layer is industrialised, frontline salesmen, who were just order takers, will have to level up the value they offer, to retain their livelihoods.

Having said that, market intelligence, retailer and distributor trust and consumer pull for brands will become the expensive layer that cannot be replicated in a hurry.

Combine this with each FMCG company’s unique go to market strategy, and we will know the winners from the losers.

Who survives

Digital didn’t kill the bank branch. It will not kill the kirana either. But it will politely and efficiently, retire the parts that were only doing the cheap work.

HDFC today, is India’s biggest bank. Central Bank of India did not survive.

Institutions that will survive will be ones that figure out which layer of value is valued by the customer and will be worth investing in.

Back to the Shekhawati merchants. They survived the onslaught of banking because they enjoyed the trust of the trader community.

But half a century later, when World War I broke out, global shipping evaporated. No trade meant no hundi, which meant no commission from money transfer.

These merchants took stock of their strengths in a time when the country was breaking free from British rule and there was a shortage of products for the local population →

- they had abundant liquid cash and

- controlled India’s domestic supply chains,

This is when they made their next strategic move towards the expensive layer of value → they moved from financing trade for goods made by foreigners, to domestic manufacturing.

That’s how the Shekhawati merchants became today’s Birla, Singhania’s, Bajajs, and Dalmias.

1 Informal promissory note

2 The trader class

3 Merchant’s seat

4 Branch

5 The largest wholesale textile market in Asia and the beating heart of Marwari financial operations in Bombay.

6 bypasses distributors to deliver stocks directly to retailers

7 lets the retailer order directly online

More ways to connect

- Strategy Activator Workshops — done with you.

We have a proven approach that we tailor to your context.

At the end of the process, you will have a strategy blueprint for growth. The approach has received great feedback from Harpic, Tata Salt and Tata Sampann. Click here to share your interest and I will get back to you.

- DIY Strategy Products

I am building self-serve products you can use to develop your growth strategy. Join the early list for first access.