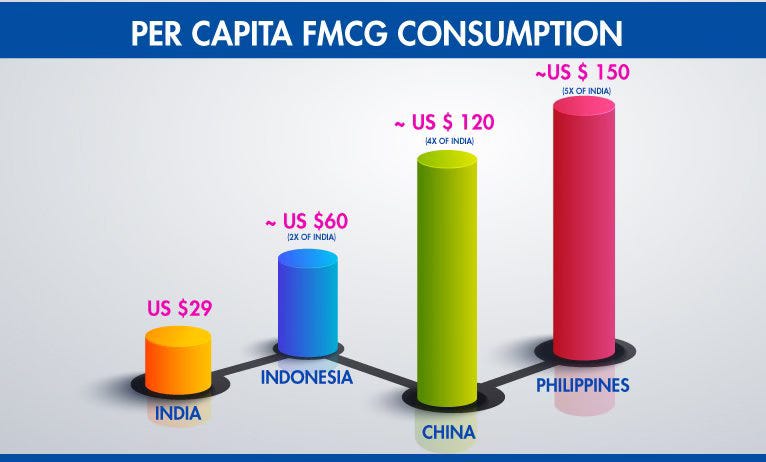

There is enough headroom to grow all FMCG categories in India.

Legacy FMCG is crawling at 4-6% growth for the last 2 years and there too, has been rescued by rural demand. D2C hits a ceiling because it can’t generate enough repeats to turn a flywheel that’s built on discounts.

Yet, India per capital consumption of FMCG has headroom to grow vs. other Asian countries.

Then why do both legacy FMCG and D2C feel ‘stuck’?

What’s going wrong?

To understand the present, I turned to the past.

2. Four insights from Carlota Perez’s thesis on lifecycles of technological revolutions

Carlota Perez1 has studied the 5 big technological revolutions that have reshaped the world over the last 240 years.

- The Industrial Revolution

- The Age of Steam, Coal, Iron, and Railways

- The Age of Steel and Heavy Engineering

- The Age of the Automobile, Oil, Plastics, and Mass Production

- The Age of Information Technology (ICT) and Telecommunications

I share four big insights from her thesis.

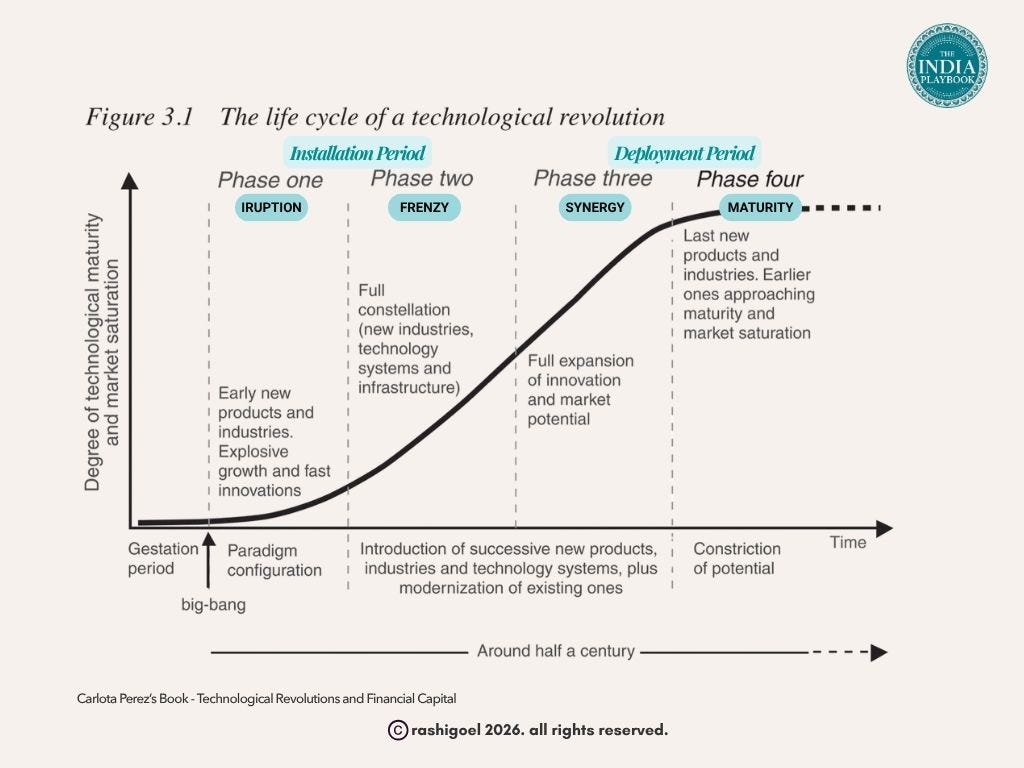

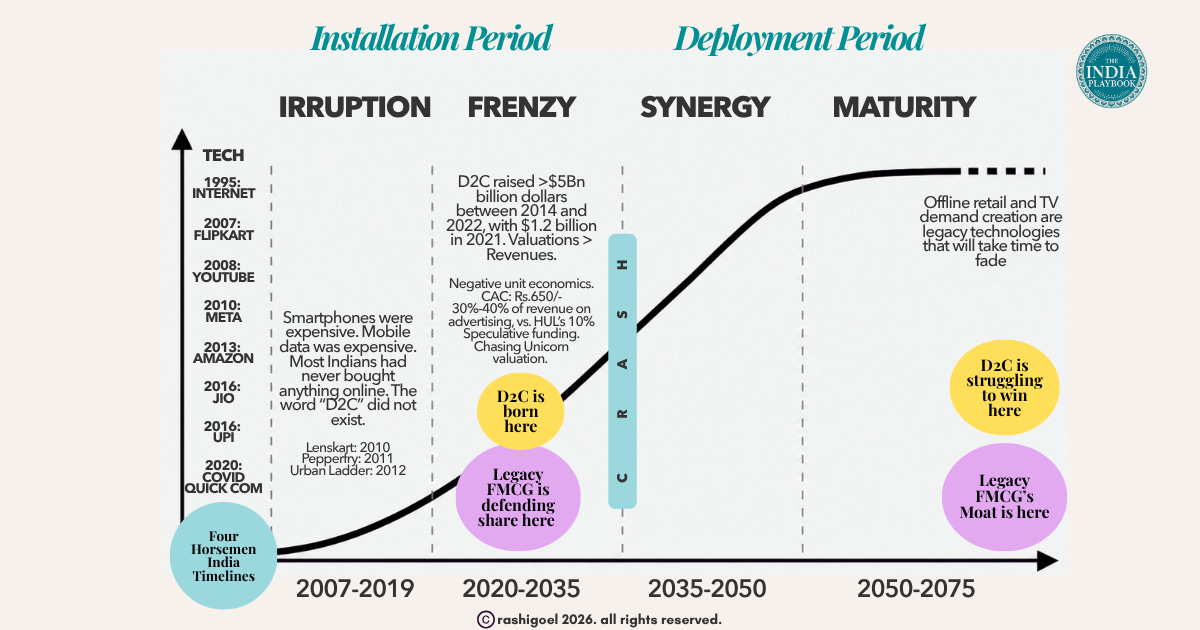

a. Each technological revolution has a 50-60 year lifecycle, divided into 4 phases

The first 30-years are a tumultuous ‘installation’ phase followed by a crash and then a 30-year golden ‘deployment’ period.

Each 30-year period is divided into two phases

→ Iruption+Frenzy = Installation

→ Synergy+Maturity = Deployment

INSTALLATION PHASE – first 30 years

1.Irruption: A new technology appears, early adopters tinker with it, most people ignore it.

2.Frenzy: as more and more people adopt the new technologies, speculative money floods in and valuations race past revenue. An economic bubble stats forming. The old and new technologies co-exist. Perez calls this the ‘Casino Period’.

CRASH. The bubble bursts. State intervenes. Infrastructure streamlines.

DEPLOYMENT PHASE- next 30 years

3.Synergy: valuations become realistic. Technology diffuses into the real economy and creates virtuous cycles. Perez calls this the ‘Golden Age’.

4.Maturity: returns diminish, and pressure starts building for the next revolution.

b. A technology revolution is never one isolated invention.

It is a bundle of technologies that create synergistic systems.

These systems only survive with the support of two more ingredients – one, enabling infrastructure, two, state governance.

When machines first mass-produced products, they relied on the canal infrastructure to ferry raw materials and finished products.

When factories needed land and workers at scale, the state stepped in with licences, labour and safety laws, minimum wages and taxes.

c. Once a technology system is in place, it creates virtuous cycles of prosperity that compound over time.

These technology systems diffuse far and wide → even beyond industries of their origin. They spawn new products and jobs, reduce cost, and propel entire economies forward.

The Industrial Revolution made it possible to mass-produce cotton, which built the textile industry, which led to fashion, which built fashion magazines and fashion shows, all the way to present day Shein, Sabyasachi and the Met Gala.

Mass-produced goods also built the FMCG industry, which in turn created the sales and marketing functions. Which in turn created the retail industry, all the way to private brands and quick commerce.

d. Technology systems become utilities.

A lot of these technologies become so ingrained into our lives that they become invisible utilities.

Electricity. Internet. Steel. Plastics. They were revolutionary when they were discovered. Today they are everywhere, but invisible → they have become mass utilities that power everything else.

All this is fine, but what does it have to offer with FMCG?

3. FMCG is not a technology, but its future is now fundamentally intertwined with technology

FMCG rides on top of technology systems → its distribution channels (kirana, modern trade, e-commerce, quick commerce), payment channels (UPI) and its media channels (social media, YouTube), are all technologies moving through Perez’s phases. So FMCG inherits the phase of whichever channel it leans on.

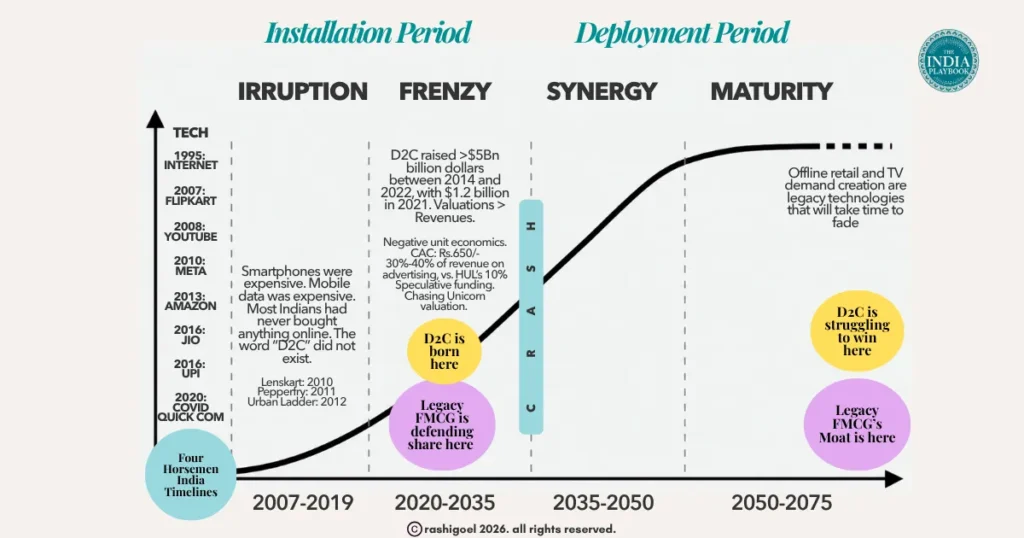

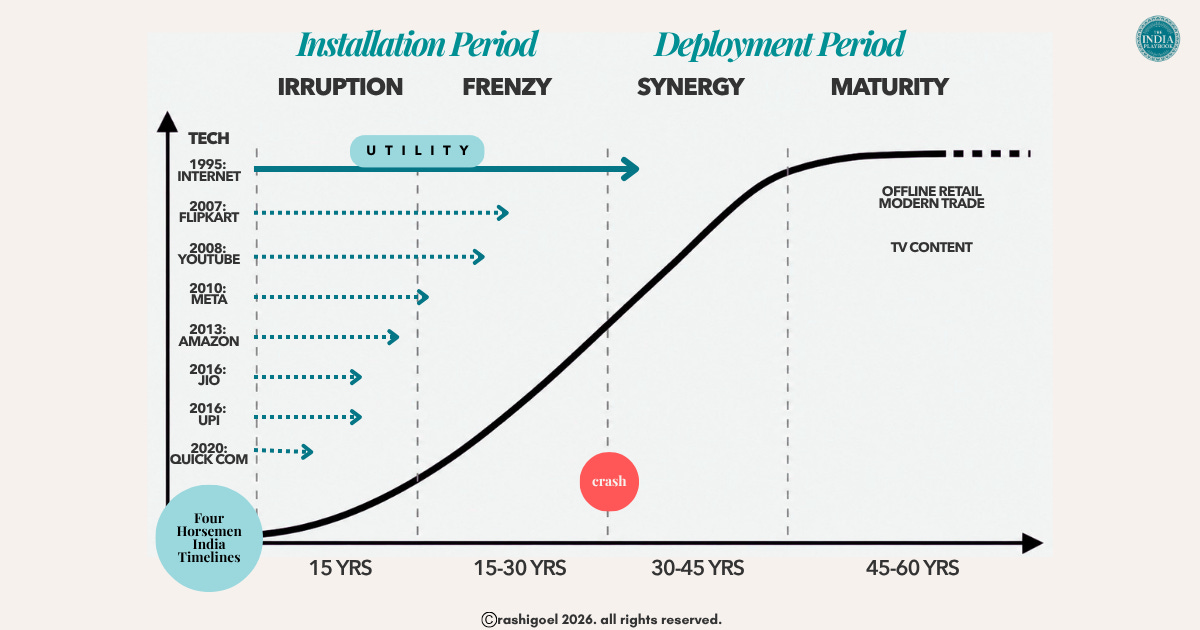

a. That’s why, the real question is. What phase are these technology revolutions in India?

In this chart, I have mapped each technology disrupter with its date of entry into India, from the Internet (1995) to Quick Commerce (2020). The horizontal arrows indicates the phase each technology is in, as of 2026.

The insights are fascinating.

- The Internet has become a utility. It entered India in 1995 and only just completed its installation phase in 2025. It is now an invisible utility like electricity, and is powering digital media and distribution technologies.

- Every other technology, from Flipkart to Quick Comm is still in Irruption and early Frenzy phase.

- The industrial age utilities of TV and offline retail distribution are in maturity phase.

b. This means is that the Great Indian FMCG industry™ is not just stuck mid-cycle, it is trying to straddle two technology turfs

D2C was born in the frenzy phase of its technologies. It will experience the volatility of these channels until they mature and enter the synergy period.

At the same time, a D2C brand that starts online caters to India 1-2 and soon hits a ceiling because 80% of India’s FMCG demand still comes from mature channels. To grow faster, it has to leverage the mature technology of the kirana shelf, A challenge that Mamaearth, boAt and Sugar have learnt the hard way, is not easy to thrive in. Yet.

Legacy FMCG’s moat is intertwined with mature technologies. It continues to stay strong in these channels and cater to India 2-3-4. But it is scrambling to defend share in the new shiny, premium, urban, online business.

To grow organically, it is reengineering its logistics, portfolio focus and media strategies. To grow even faster, it is resorting to strategic buy-outs of D2C brands.

In short, both are straddling a huge technological transformation between old utilities (TV, kirana, modern trade) → mature, not fading fast, and new ones (e-commerce, quick commerce, digital media) that are still in frenzy phase and volatile.

c. As they copy each other’s playbooks. they mimic only what’s visible which makes them strategy blind™.

Both started with different moats and now both are building a plane while flying it. Each started with one playbook for one turf — D2C for the frenzy channel, legacy FMCG for the mature one. Now both are trying to bolt the other’s playbook onto their own, so they can win in both the turfs.

Both began from opposite start points, so their culture, instincts and ways of working are poles apart. As they iterate their playbooks, their people, culture and systems will have to iterate with them also, and that’s as hard as asking a cricket team to play an IPL match in the morning and compete in a gymnastics tournament in the afternoon; and to do this day-after-day.

That’s why they are flying strategy blind™.

This is the most important insight – a playbook isn’t a deck. It is tacit knowledge that cannot be copied. It can only be grown from scratch. When each bolts on the other’s playbook, it copies the visible parts, the dashboards, the org charts, the job descriptions, and misses the invisible tacit knowledge that actually makes each playbook work.

So both end up running the other’s playbook strategy blind™, i.e. mimicking the actions minus the craft underneath.

d. There is hope. Because we’ve seen this movie before.

For most of the 1800s, FMCG was sold loose. Grocers kept unbranded and loose products in barrels, drums and sacks – flour, dal, soap, washing powder, milk, ghee, biscuits. The grocer was the brand. He recommended products to consumers, told them how to use them, and even gave them credit.

Then Dabur (1884), Lever Brothers (1885) and Britannia (1892) started mass producing sealed, packaged goods. They bypassed the grocer to create demand directly by advertising in magazines and radios.

The new brands had better products but lower margins. Yet, they had to convince the very grocers they were disrupting to stock their products.

The grocers fought to keep their margins. But they had to give in when more and more consumers started asking for brands by name.

It has taken 142 years, from Dabur’s founding in 1884 to today, for the mass-produced branded disruptors of yesteryears to become todays’ legacy FMCG industry which is now being disrupted too.

The lesson is that survivors went through the friction and built their own playbooks from the ground up.

The grocers survived because they kept pace with FMCG moves. And FMCG survived because it kept adapting to the license raj, modern trade, demonetisation, covid, and GST.

Which is exactly why copying the other side’s playbook faster is strategy blindness™. Each will go through trial and error and will grow their own playbook for both turfs. The sooner they do that, sooner they will get ‘unstuck’.

Sources

- Carlota Perez, Technological Revolutions and Financial Capital (2002); Technological Revolutions and Techno-Economic Paradigms (2009 working paper).

1 scholar of technology and socio-economic development

Two ways to stay in touch

- Strategy Activator Workshops — done with you.

A proven approach that we tailor to your context. At the end of the process you will have a strategy blueprint for growth. The approach has received great feedback from Harpic, Tata Salt and Tata Sampann. Click here to share your interest and I will get back to you.

- DIY Strategy Products

I am building self-serve products you can use to develop your growth strategy. Join the early list for first access.