Two playbooks dominate the consumer goods market in India right now.

Playbook 1 exploits its legacy cash cows and wants slow and steady growth.

Playbook 2 is impatient and will do anything to grow exponentially.

Both rely on safe and hyper-rational, therefore incremental ideas.

Neither offers value that’s aligned to their zone of mastery, i.e. a value proposition that is unobvious, unreplicable, unboring, and with the potential for uninterrupted compounding.

Here goes.

- Playbook 1: Legacy businesses

- Playbook 2: D2C businesses

- Playbook 3: The Zone of Mastery way

Playbook 1: Legacy businesses

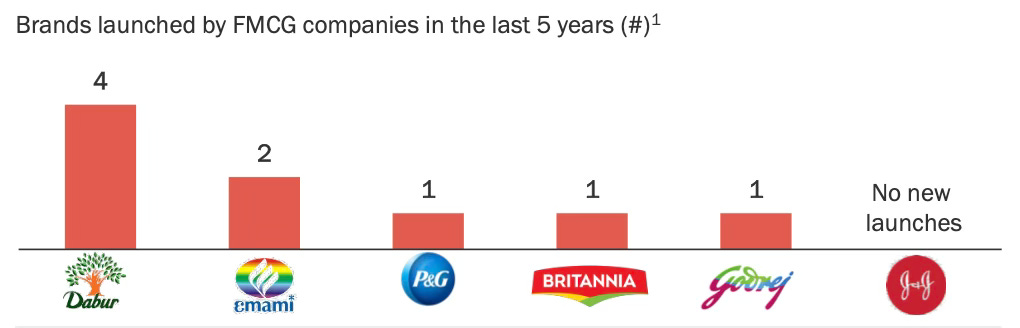

Legacy businesses juice out their two moats – distribution and brand strength – built over decades, if not centuries.

This gets them to that magic Rs.100 crore ($12 million) topline faster than any D2C business.

On the flip side, they are also risk-averse.

Who suffers? Marketers. They are caught between a rock of great ideas throttled by a bureaucratic system and a hard place of mindless number crunching to justify and ‘sell’ their plans to sales teams.

This unwillingness to fail fast by putting more products out there has opened up various white spaces that D2C brands are entering.

For instance,

Lenskart, Zivame, HRX and Licious solve for a poor offline shopping experience and lack of variety.

Sugar Cosmetics, Bombay Shaving Company, BoAt, and Mamaearth solve for innovative product and price combinations where legacy brands are absent.

Traya, Cult Fit and Phool solve difficult problems by bolting together innovative product+service bundles and new business models.

Country Delight, The Whole Truth, and YogaBar solve for adulteration, health and convenience.

Some of these businesses, in my opinion, are operating in a zone of mastery.

When we look beyond this handful of companies, we see that the D2C playbook is a cookie-cutter one.

Playbook 2: D2C businesses

The D2C business playbook anchors on chasing valuations.

Companies raise multiple rounds of higher and higher valuations, each engineered to drive up exit valuations.

Founder CEOs need to increase topline growth exponentially to justify higher valuations in each round.

However, because of three peculiarities of the Indian market, they face demand-side constraints.

- Offline distribution is fragmented, so until the company’s turnover crosses Rs.100 crores ($12 million), its distribution footprint is limited to E-Commerce.

- The growth potential from an underpenetrated consumer market of 1.4 billion looks huge. But when we dig a little deeper, we see that there are no more than 110-150 million online shoppers.

- 90% of whom are cash-poor.

This leads to a supply-side glut of copycat brands fighting over the same consumer wallet.

The proof lies in Amazon search results. Search for any consumer good, and you get hundreds, if not thousands, of results. All look similar and profess to benefit you in the same exact way.

Let’s take the 389 peanut butter products on Amazon as an example. We find ourselves swimming in a peanut-flavoured sludge of green, yellow and white jars, each labelled with a combination of the exact same five words—unsweetened, crunchy, creamy, protein, and natural.

Even if we were to believe that all of the richest Indians shop online, how many brands of peanut butter do they need?!

Amazon, Big Basket, and Blinkit are great equalizers—all products have the exact same square footage on the home page window.

Faced with this commoditised selling arena, brands can either hope to get lucky (never a good strategy in the long run) or ‘buy’ sales through discounts and performance marketing, which drives up Customer Acquisition Costs (CAC) month on month.

Is it surprising that missed growth targets have led to a rationalisation of investments?

Who suffers? Marketers. They are caught between a rock of justifying ROAS on e-commerce spending and a hard place of justifying ROI on advertising spending.

Playbook 3: The Zone of Mastery way

This playbook starts right at the beginning and clarifies three questions for each business:

1) Who am I?

No two founders are alike. Their experiences and personalities make them unique. This playbook starts by looking at why the business exists in the first place. It knits the founder’s DNA into the business raison d’être, so the origin is not just personal but also inimitable.

2) What do I offer that no one else can?

This playbook sees what’s already there with fresh eyes and then connects the dots in unobvious ways. This results in a value offer that is fundamentally different, not just incrementally better.

3) How do I boldly declare the value that I provide?

Thoughts don’t build great businesses. Actions do. This playbook recommends tangible, bold and unboring go-to-market actions. It feels risky because, most likely, some actions have never been done before.

This playbook creates entire markets, even industries from scratch instead of being ‘dictated’ by the market.

Both challenger and legacy brands can adopt this playbook.

It shapeshifts according to the business, category and context. That’s why there are as many zone of mastery strategies as there are businesses.

Here are a few I have written about – Lemonade, Mokobara, Traya, Cult Fit and Phool.

Thanks for reading and I’ll see you next week.